Maybe no-one in your fundraising office would say “So What?” but that does not mean they are not thinking it. What is the big deal about public company insiders and how can you succinctly convey that relevance in conversation – or even profiles? I have three things to say about that!

1. Years of Growth (or not)

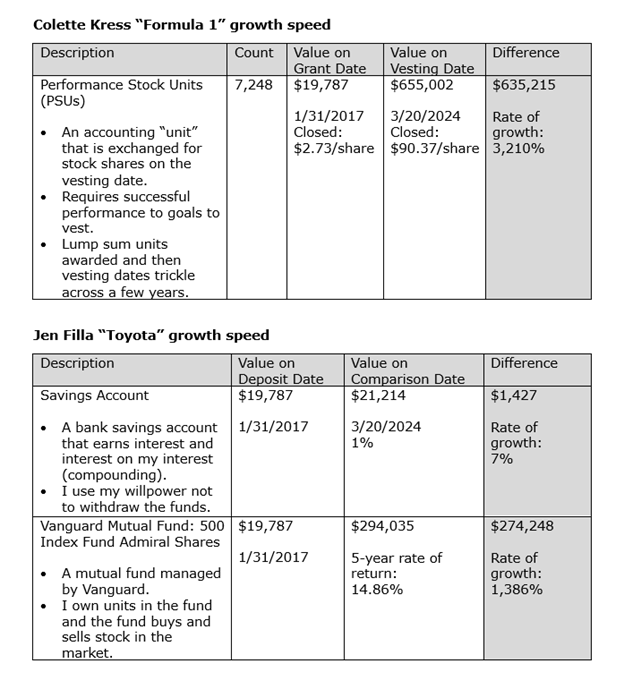

Especially during economic volatility, a 5-year or 10-year chart of stock performance can visually demonstrate whether your insider is experiencing heady wealth accumulation – or not.

Because your insider is likely getting paid a cash salary and a cash incentive/bonus, those stockholdings represent long-term incentive and they grow at rates your savings account can merely fantasize about.

That means that if the stock price chart is moving up significantly in value, your insider’s stockholdings are highly appreciated assets that are untouched by living expenses.

What is that stock price chart? Oh that. That is your insider with “excess” assets making great rate returns.

2. Gifts of Stock

I do not know what percentage of insiders make gifts of stock, but at Aspire, we find a good portion of the insiders we research make gifts of stock. However, it is not always to an operating nonprofit.

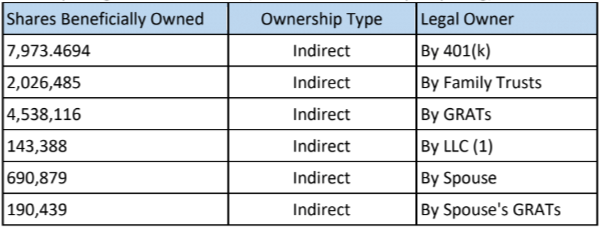

But many times the stock is gifted to a family foundation, which is significant, or to a family trust, which is, again, excess assets making great returns.

Regardless of who the stock is being gifted to, the key point here is that the insider has the knowledge and maybe even has the habit of gifting stock.

When you reach a deeper relationship and the insider is keen to make a significant investment in your organization’s work, gifting stock may be an option your prospect already uses – no education required.

3. Counting Cashed Out Stock

It is possible to skim through the insider’s Form 4 filings for specific file types that indicate which sales of stock resulted in cash in the insider’s pocket. But you have your work cut out for you untangling them from all the sales of stock used to exercise stock options, pay taxes, or other sale types.

Aspire recently subscribed to Kaleidoscope’s Insider Focus research tool and it is the perfect use for A.I. The software has no problem making the calculations to tell me exactly how much stock was cashed out during a specified time-period.

This is an amazing number! Did your prospect cash out stock to the tune of millions of dollars in the past year or two? Now you can know with a click!

Knowing that this cash is above and beyond salary and bonus gives you a snapshot of what kind of money is “psychologically” available. In other words, it is money that the insider is already comfortable cashing out of stockholdings.

Even if this cash is being invested elsewhere, it gives you a sense of how much money could be available if the insider is deeply motivated.

When someone is an insider it is a good bet there’s significant wealth

For at least the three reasons above, if you are trying to identify $1 million+ potential donors for your campaign, or otherwise trying to spot the most capable prospects in your donor base, do not underestimate the insiders!

Money is never enough, of course. Prospects need to have an interest, be philanthropic, and be reachable, but there is no doubt that big visions need big money.

Do you need to learn to read SEC filings?

If you are looking for training on how to assess public company insider wealth from Securities and Exchange Commission (SEC) filings, check out the training offered at the Prospect Research Institute!

Curious about compensation and beneficial ownership, but also how to incorporate into capacity and the profile? This 3-workshop bundle has you covered! Enroll Now

Additional Resources

- Insiders and the Paycheck that Keeps Payingv | Jennifer Filla | Feb 2025

- Why Insiders? | Elisa Shoenberger | Aspire Major Gift Insights | Feb 2025

- Why Do Insiders Disclaim Beneficial Ownership? | Jennifer Filla | Jan 2021

There was a cry for help on the PRSPCT-L list-serv: “I’m a new researcher and my boss wants me to provide net worth on a prospect. He says it was the previous practice to do this and I can get what I need to calculate it from Dun & Bradstreet.” What would your response be?

There was a cry for help on the PRSPCT-L list-serv: “I’m a new researcher and my boss wants me to provide net worth on a prospect. He says it was the previous practice to do this and I can get what I need to calculate it from Dun & Bradstreet.” What would your response be?