If you are a prospect research professional, odds are that you have searched for the beneficial ownership of securities table in a proxy filing with the SEC. But do you really know what beneficial ownership means Why do insiders sometimes disclaim the beneficial ownership they reported? Should you care? Maybe. If you have to explain it to others, such as development officers, then definitely!

The proxy (Form Def 14a) is the document a public company files each year to explain and be transparent about the securities or stock it has on offer for purchase by the public. After all, the SEC came into existence in 1933 to restore investor confidence in our capital markets after the stock market crash of 1929. From that perspective, beneficial ownership makes a little more sense.

A beneficial owner is…

- A person who enjoys the BENEFITS of ownership even though the stock is not directly owned in his/her name.

For example, I may change the title of my stock to a trust, or a foundation, or an LLC, but still, maintain the benefit of ownership as a trustee or beneficiary or both.

. - A person (individually or as part of group) who has the power to vote on shares, or who wields influence over a shareholder’s vote.

Fundraising research is less concerned with whether the prospect can influence the votes of shareholders, but we do care about enjoying the BENEFITS of ownership, because this can have an impact on our prospect’s wealth picture.

James Dimon Example

Let’s look at an example: James “Jamie” Dimon is CEO of JP Morgan Chase & Co. (JPM). According to the beneficial ownership table in the proxy filed on 4/6/2020, he owns 9,538,667 shares of company stock. Or does he?

Footnote #3: Includes 115,800 shares owned by entities as to which Mr. Dimon disclaims beneficial ownership, except to the extent of his pecuniary interest therein.

If Mr. Dimon BENEFITS from those 115,800 shares, but DISCLAIMS this beneficial ownership, who might have legal and direct ownership of them?

A Form 4, Statement of Changes in Beneficial Ownership, must be filed every time an insider has a change in the number of beneficially owned shares. It often gives us greater detail on who owns exactly what shares. Could it help us with Mr. Dimon’s disclaimed, mystery 115,800 shares? Indeed, it does!

Form 4| Filing date 10/14/2020(much later than the proxy filing

Note the footnote #1 next to ownership by “LLC”? This savvy guy doesn’t want us to know the name of the LLC, just that it is an LLC.

Footnote #1 reads: Reporting person [James Dimon] disclaims beneficial ownership of such shares except to the extent of any pecuniary interest.

Mystery solved?

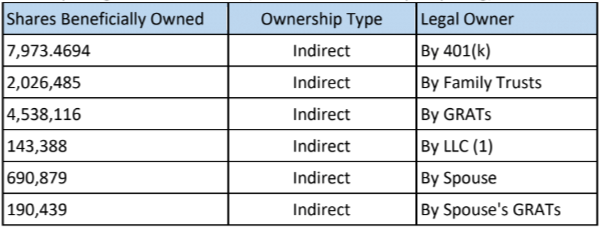

An LLC of undetermined name legally owns title to 143,388 shares of JP Morgan Chase & Co. stock. And Mr. Dimon DISCLAIMS that ownership, even though he is legally required to report it because he benefits from the ownership.

Translation / Interpretation

In Mr. Dimon’s example above, we are discussing fewer than 200,000 shares out of more than 9 million shares. From that perspective I care a lot less about that mystery LLC. But I have researched more than one prospect where the mystery LLC owns the lion’s share of stock. Sometimes I even know the full name of that LLC.

And too often, even knowing the company name doesn’t help.

As I have described before, someone like Mr. Dimon could be a member of an LLC in Delaware and the public (and even the Delaware Division of Corporations) wouldn’t know it!

The DISCLAIMING of beneficial ownership in Mr. Dimon’s case feels interesting because he benefits from a laundry list of indirect ownership that he does not disclaim: 401(k), family trusts, spouse, etc. Since he does indicate a pecuniary (financial) interest in the LLC shares, we might speculate that he expects to profit from whatever the mystery LLC is going to do with his shares, but that he argues that he is not influencing the investment.

Is Speculation Warranted?

Speculating is fun! And sometimes it does help to put numbers into perspective, especially if you are fussing over exactly how much and what kind of gift proposal to put together for a prospect.

Following is my completely fictional speculation about Mr. Dimon’s mystery shares as written for the prospect profile. For this fictional example, assume that I discovered the name of the LLC was MiamiBeach LLC and that I knew his daughter started a real estate venture in Miami Beach.

We know that Mr. Dimon’s 32-year-old daughter recently began a real estate venture in Miami Beach, Florida. We do not know who owns Miami Beach LLC because it was incorporated anonymously in Delaware. Since Mr. Dimon disclaims ownership of the shares owned by Miami Beach LLC, we might speculate that it is his daughter’s company, and that Mr. Dimon invested those shares in his daughter’s company, expecting a financial return.

We can speculate, be we can’t actually KNOW this to be true. The information about the true disposition of those shares is NOT available to confirm our speculation.

Be Clear. Be Firm. Have Fun!

If you are going to pick apart stock holdings and speculate, just be sure to use very clear language. Words such as the following are useful:

- We do NOT know if this is true, but we are GUESSING based on…

- We can NOT know who owns this company, but we SPECULATE…

- Mr. Dimon disclaims his ownership of these shares and although we can NOT know the details of exactly who owns the shares, we SPECULATE…

- Because this is SPECULATION, you might want to consider these shares as NOT available for gifting.

The pressure on your development officers to raise the most money possible to further your mission is real and it is powerful. If you are comfortable speculating, it can help your development officer to put the stockholdings into perspective relative to the full philanthropic and wealth picture of the prospect.

But there is a limit to what we can know. And when the prospect has deliberately placed information beyond public viewing, it is worth stating. After all, our prospects are just as entitled to their privacy as we are. To attempt to pull back the veil of privacy could be construed as disrespectful with the potential to damage the relationship.

I enjoy the tangled web of financial filings and the constant rebalancing of how exact to attempt to be when presenting the information. I hope this example made beneficial ownership just a little bit clearer.

Additional Resources

- Want to dive in deep to insider SEC filings? Become a member and enroll in the Insider Stock and Compensation Course. >>Learn More

- Wish you had an SEC filings reference book handy? Purchase the Insider Stock and Compensation Workbook and focus on filings and information that matters for fundraising. >>Learn More

- Can You Really Hide LLC Ownership? You Betcha!| Jennifer Filla | 2020